Online net banking has emerged as the primary mode for Indian customers to access banking services due to its numerous advantages in the digital era.

This is why:

- It offers convenience, allowing customers to access their accounts and carry out transactions anytime, anywhere, without the need to visit a physical bank branch.

- It provides a wide range of services, including fund transfers, bill payments, and investment options, all at the click of a button.

- Card and cash-based transactions have limitations, such as the risk of loss or theft, the number of merchants accepting card-based payments being limited, and the hassle of failed transactions.

Net banking overcomes limitations by providing a secure and efficient platform for customers to manage their finances, making it the preferred choice for Indian customers seeking a seamless digital banking experience.

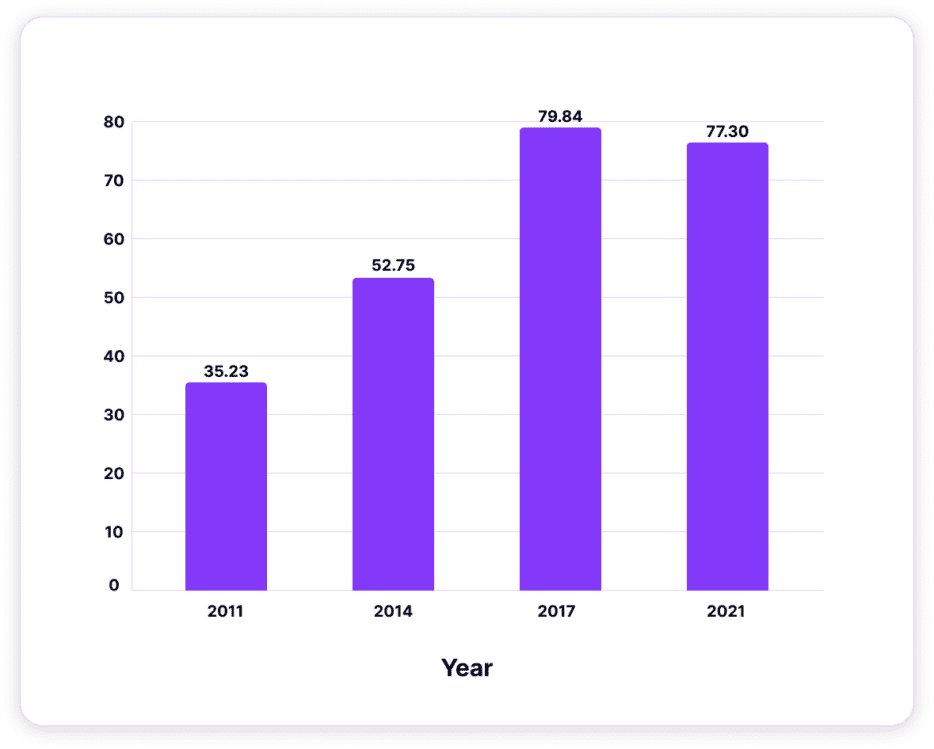

Source: theglobaleconomy.com

So, what has changed in the last decade?

The adoption and availability of smartphones and reliable high-speed 4G connections have improved the landscape dramatically within the last decade.

This, along with the launch of the Unified Payments Interface (UPI) in 2016, led to the rise of e-wallets and mobile payment applications.

What is UPI?

UPI is a real-time payment system introduced by the National Payments Corporation of India (NPCI). It enables individuals to link multiple bank accounts to a single mobile application, making it easy to initiate peer-to-peer (P2P) transactions or make payments to merchants.

With UPI, users can send and receive money using a unique virtual payment address (VPA) instead of bank account details, reducing the need for traditional payment methods. UPI leverages mobile devices and internet connectivity, enabling users to make payments 24/7.

It has been widely adopted in India, promoting digital payments and financial inclusion by offering a simple, secure, and efficient payment mechanism.

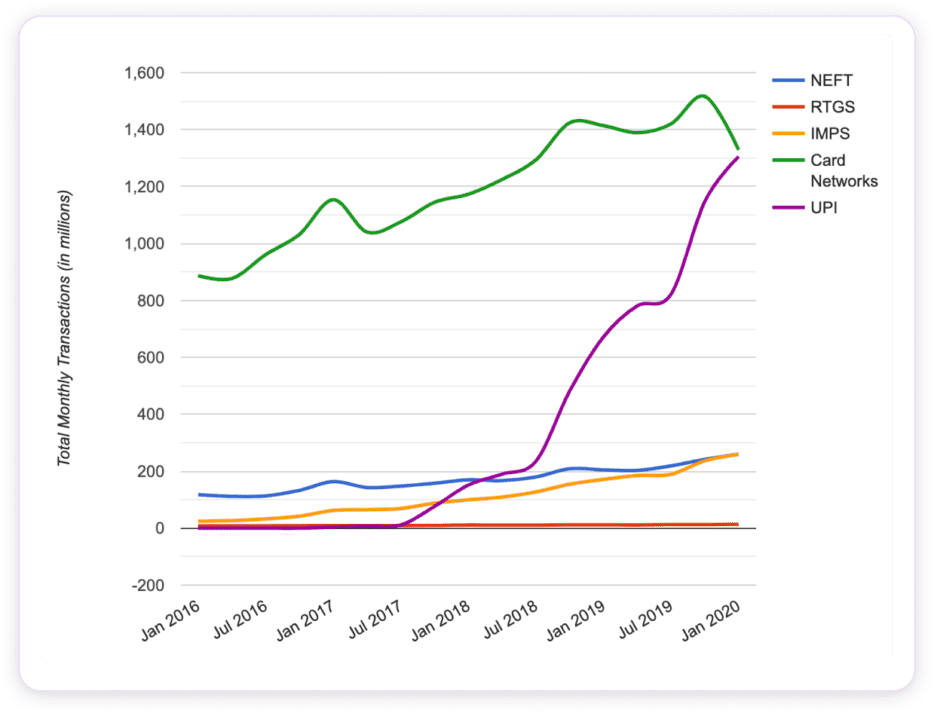

See below the scale of adoption in this simple graph:

Source: setu.co

Where do APIs fit into all of this?

APIs are core to the UPI as they form the technological foundation that enables seamless communication and interaction between different entities within the UPI ecosystem.

Here’s how:

- Transaction initiation: UPI APIs allow users to initiate payment transactions.

- Fund transfer: API integration enables the transfer of funds between the sender and receiver’s bank accounts.

- Authentication and authorization: APIs play a crucial role in authenticating users and authorizing transactions also with 2FA.

- Transaction status and history: UPI APIs provide functionality for retrieving transaction status and history.

- Integration with third-party apps: UPI APIs allow integration with third-party applications, such as mobile banking apps, e-commerce platforms, and payment service providers.

- Interoperability: UPI APIs ensure interoperability by adhering to common API standards.

What does this mean for the banking backend systems?

Banks are changing their backend systems to integrate with and support the Unified Payments Interface (UPI) in many ways, but we will see the two key ways this is changing their backend systems.

- UPI API Integration: Banks are implementing UPI application programming interfaces (APIs) provided by the National Payments Corporation of India (NPCI). These APIs enable banks to connect their existing systems to the UPI infrastructure, allowing seamless communication and transaction processing.

- UPI payment gateway: Banks are setting up UPI payment gateways within their backend systems. These gateways act as intermediaries between the banks and the UPI ecosystem, facilitating the secure transfer of funds and transaction verification.

How are the banks performing?

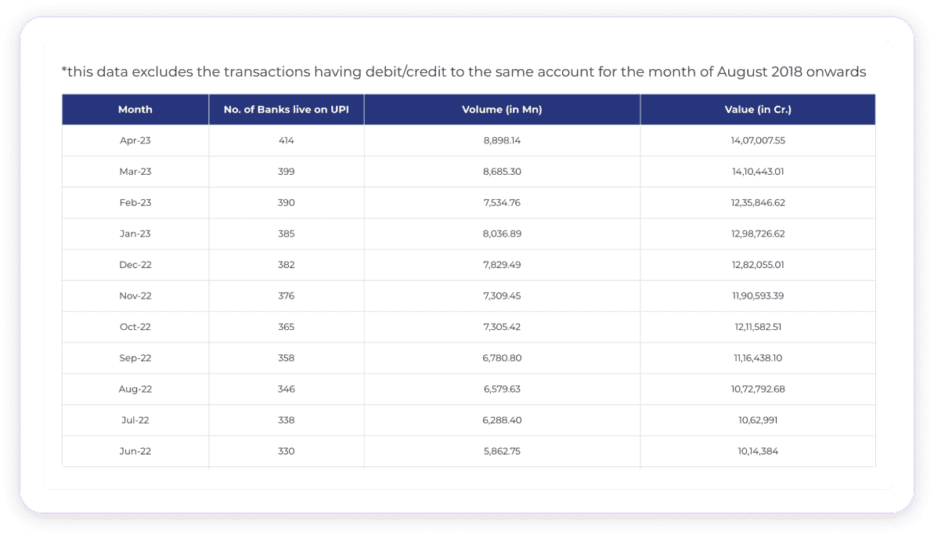

A picture can speak a thousand words. See this table below for the volume of traffic only on UPI transactions and the actual value.

Source: www.npci.org.in/what-we-do/upi/product-statistics

The above table gives you a clear picture of the number of banks adopting UPI, changing their backend systems and the volume they consume. This figure relates only to the UPI transactions they handle monthly, but the number of internal or backend transactions they reach should also be skyrocketing.

Performance is critical for UPI transactions as it ensures a seamless user experience, real-time transaction processing, customer trust, competitiveness, volume handling, and regulatory compliance, enhancing the efficiency and reliability of the payment system.

Indian banks are adapting their backend systems to accommodate the Unified Payments Interface (UPI) in several ways. They are going through a massive digitisation process and overhauling their backends to accommodate the spike in API traffic.

Enter Tyk

As the banking sector in India continues to embrace digital transformation and open banking initiatives, the need for secure and efficient API management becomes paramount. Tyk’s API Gateway provides a robust and scalable solution that enables banks and financial institutions to streamline their API operations, ensuring seamless connectivity, enhanced security, and effective management of APIs.

With its lightweight and efficient design, optimised routing algorithms, and scalable architecture, Tyk can handle high API traffic volumes, provide fast response times, and ensure reliable and efficient communication between clients and backend services.

If you want to know more about leveraging Tyk’s advanced features and capabilities to harness the power of APIs, speak to one of our expert engineers here.